OVERVIEW

The U.S. stock market, as measured by the S&P 500 index, rose about three percent last week.

Large-cap stocks with a growth orientation led the way higher. In particular, the tech-heavy Nasdaq Composite gained over six percent.

Developed country stocks did less well, gaining just 0.75 percent. Emerging market stocks did better, though, rising nearly 1.5 percent.

The yield on U.S. 10-Year Treasury notes fell to 0.64 percent, resulting in gains for long-term Treasuries.

Both high-yield and investment-grade bonds showed price increases of over two percent.

Commodities were down by more than two percent across the board, dragged lower by oil, gold, and grain prices.

KEY CONSIDERATIONS

A Tale of Two Markets – Although many of the stock market sectors were negative last week, the S&P 500 index, which represents the stocks of the 500 largest companies in the United States, still gained about three percent. This was mainly due to substantial gains in consumer discretionary and tech stocks, both of which have benefited from an economic environment full of quarantined consumers.

The S&P 500 index is capitalization-weighted, meaning the weight of each stock in the index is determined by the total market value of its shares. So when a few companies accumulate massive market values, such as the big tech names, they represent the majority of the movement within the index.

By contrast, the S&P 500 Equal Weight index gives all 500 companies in the index an equal weighting. So if we compare the performance of the two indexes to each other, we can see just how much the largest companies are outperforming the rest of the pack.

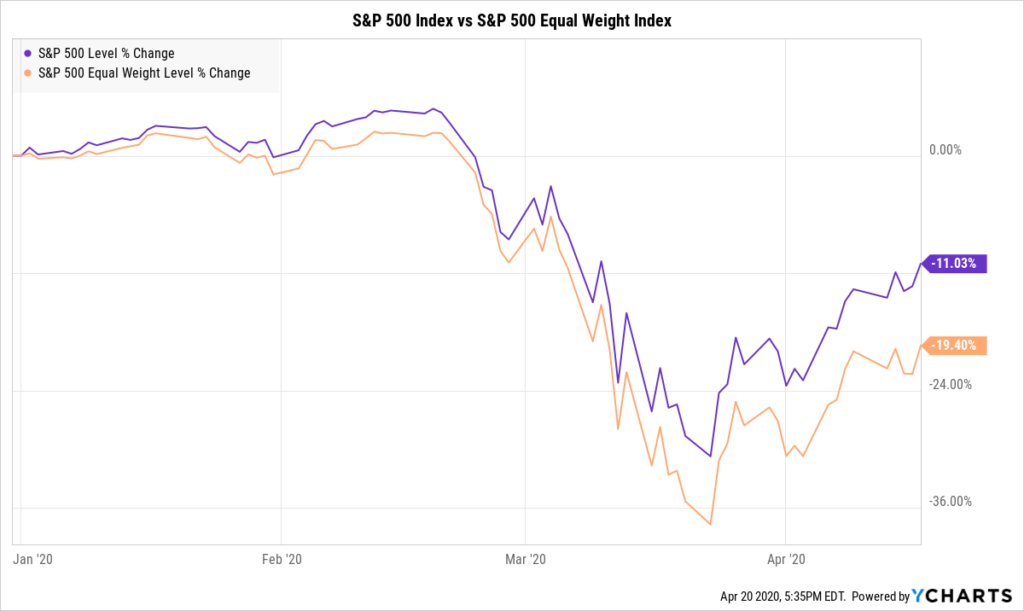

Indeed, as the following chart shows, the S&P 500 index is down over 10 percent this year. The S&P 500 Equal Weight index, however, is down nearly 20 percent.

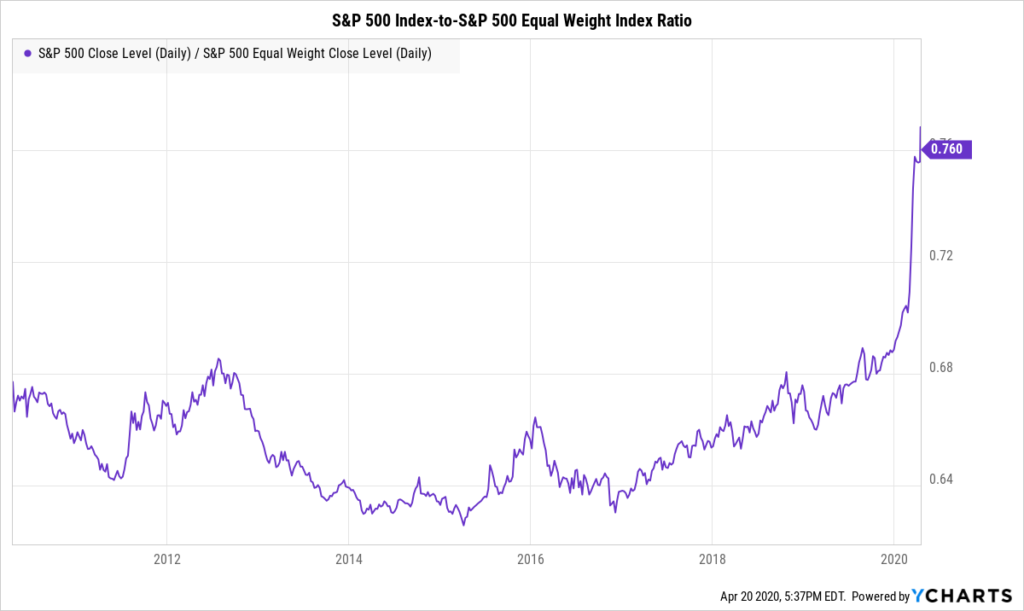

Viewed differently, the next chart shows the ratio of the closing price of the S&P 500 to its equal-weighted counterpart over the past ten years. The ratio has been on an uptrend since the end of 2016 but really accelerated during this recent sell-off. In other words, the big tech names are outperforming even more than usual.

So we find ourselves in a kind of segregated market, with the winners flourishing and the losers floundering.

Many of the small businesses that aren’t publicly traded probably won’t make it to the other side of this crisis intact. As for the big companies, the major airlines have already received government bailouts. And we have heard of some big retailers exploring bankruptcy options.

Warren Buffet once quipped that when the tide goes out, we find out who’s been swimming naked. After a long bull market, this crisis could be the catalyst that thins out the herd. As for the fittest in the pack, they appear to be getting even stronger.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.