OVERVIEW

U.S. stocks fell for a second week in a row last week, with the S&P losing 0.3%, the Dow dropping 0.88%, and the Nasdaq declining 0.28%.

The Russell 3000 Growth Index, a broad gauge of growth stocks in the U.S., fell 0.94%, whereas its value counterpart rose 0.16% for the week. Small-cap stocks also did well, gaining about 0.28%.

International stocks fared better. Developed country stocks rose 0.17%, and emerging markets jumped 2.56%.

Bonds had another poor week as the 10-year Treasury yield rose to 1.79% by week’s end. Short-term Treasuries remained roughly flat, intermediate-term Treasuries fell 0.13%, and long-term Treasuries dropped 0.02%. Investment-grade bonds fared worse, falling 0.44%, whereas high-yield (junk) bonds managed to gain 0.07%. Municipals fell 0.48%, and TIPS dropped 0.25%.

Real assets were mixed for the week. Real estate lost about 1.4%, but commodities gained around 2.2%. Leading the way was oil’s 5.8% gain, followed by gold rising 1.17%. Corn fell about 1.7%. The U.S. dollar weakened by about 0.62%.

KEY CONSIDERATIONS

Looking Backward and Forward – Earnings season is here again, which means companies are releasing their earnings results for the last quarter of 2021.

Most signs point to it being a good one. Not as good as the past three quarters but still good; analysts expect the year-over-year growth rate for Q4 earnings to come in around 20%.

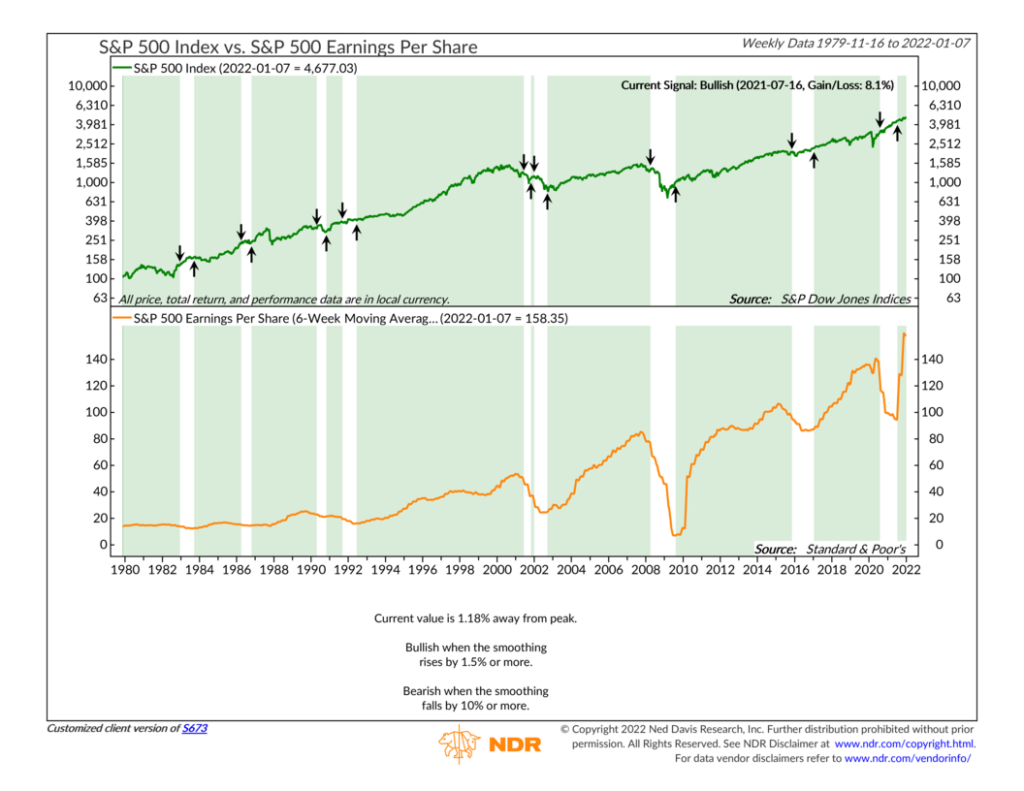

Looking at the 6-week moving average of S&P 500 earnings per share over time (shown on the chart below), we can see that stocks tend to do well when earnings are growing strongly—as they currently are.

This chart goes a long way towards explaining how we got to where we are today in the stock market.

Earnings growth was just stellar last year. For 2021, S&P 500 stocks are estimated to have grown their earnings per share around 45% from the prior year. That’s a much higher growth rate than the roughly 27% gain for the S&P 500 index last year, which means the price-to-earnings ratio of the S&P 500—a measure of valuation—came down quite a bit.

So, looking in the rearview mirror, it was an exceptionally good year for equity markets overall.

However, as we look ahead, there are some signs that the corporate earnings environment could be less exceptional—and probably more “normal” going forward.

For example, industry analysts expect earnings to grow about 8.5% in 2022 and another 10% in 2023. Add in a percent or two for dividends, and that would be a nice return for the S&P 500. That assumes, however, that the multiple investors are willing to pay for earnings—the P/E ratio—stays constant.

That’s a wildcard. And it will be even more of a factor in a year like 2022, in which the Fed intends to raise interest rates to curb inflation.

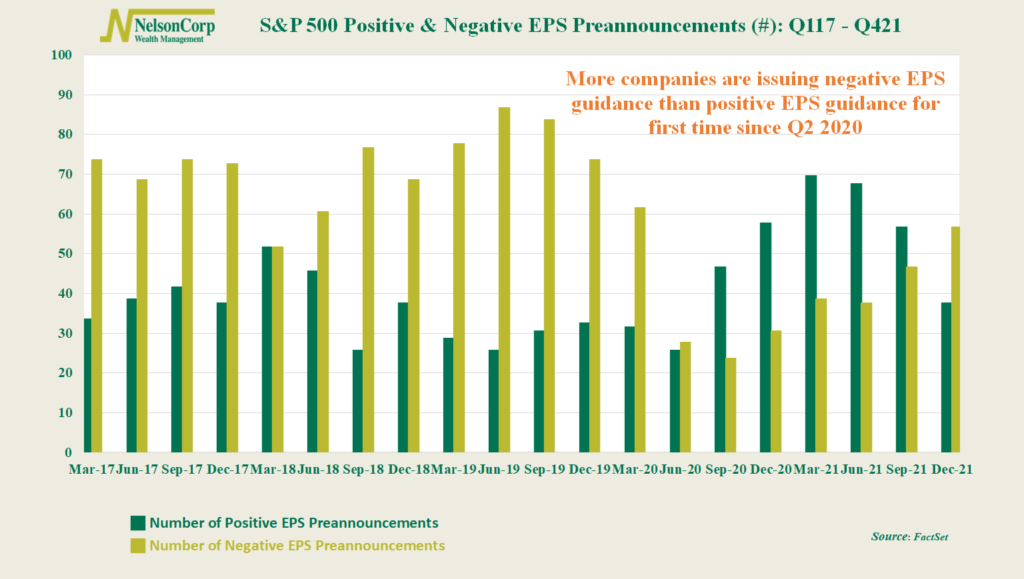

Companies are already trying to set expectations. The chart below shows that the number of S&P 500 companies issuing negative earnings guidance for the fourth quarter is 56. The number giving positive guidance, however, is only 37.

Not since the second quarter of 2020 have more companies issued negative earnings guidance than positive earnings guidance in a quarter.

Looking at the chart, however, you’ll notice that this is actually pretty normal. Over longer periods of time, more S&P 500 companies tend to issue negative earnings guidance than positive earnings guidance. So, this is just another sign that the earnings environment is returning to a more normal environment.

So, overall, the main takeaway is that although we had a great earnings year for stocks, it probably won’t continue at such a phenomenal pace in 2022. To be sure, earnings growth will still likely be a positive return factor for stocks in the coming years. But if earnings come in lower than expected, and/or investors are forced to reprice risk due to higher interest rates, it could mean returns for stocks will come in lower than what we have grown accustomed to in the past few years.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.