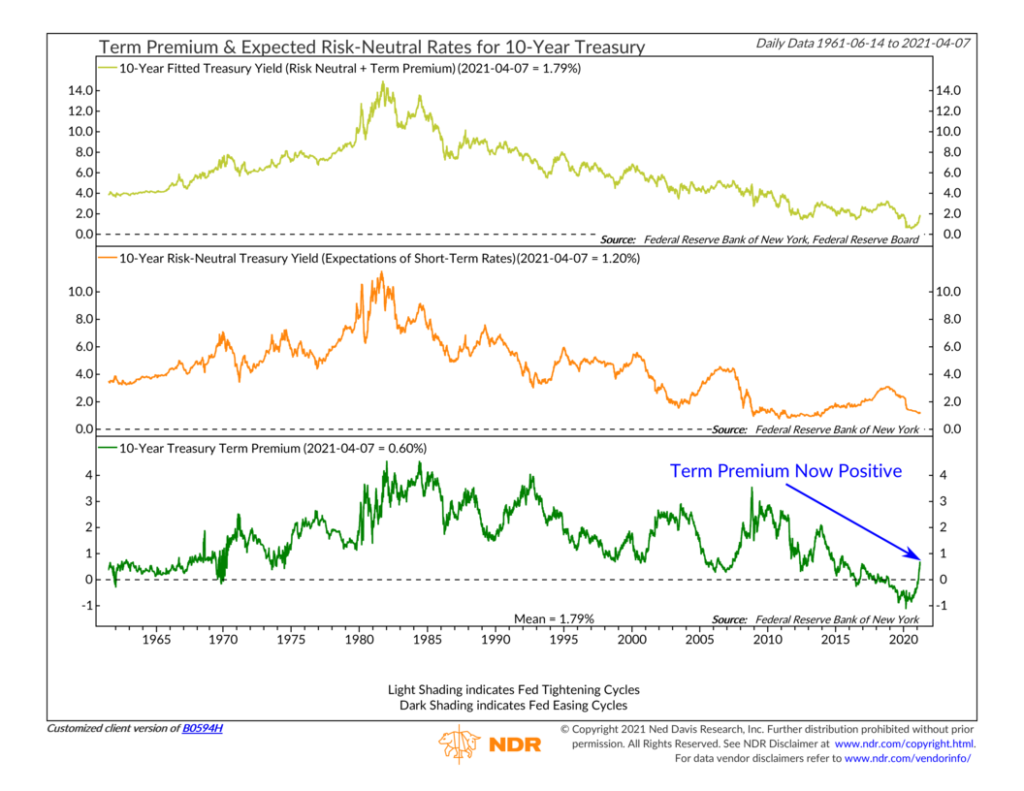

For this week’s chart, we focus on the bond market and what is called a “term premium.”

But before I describe the term premium, I’ll explain the layout of this chart. In the top clip of the chart, we show the yield of the U.S. 10-year Treasury note. In the middle clip is the 10-year Risk-Neutral Treasury yield (which I explain later). And in the bottom clip is the 10-year Treasury Term Premium. (If you add the term premium in the bottom clip to the risk-neutral yield in the middle clip, you get the 10-year Treasury yield in the top clip.)

So, what’s the term premium? In simplest terms, a term premium is an extra return that lenders demand to hold a long-term bond instead of investing in a series of short-term bonds. To understand what this means, it’s helpful to decompose a government bond yield into three components: expected inflation, expectations about the future path of real short-term interest rates, and a term premium.

Expected inflation is straightforward. Inflation reduces the purchasing power of future cash flows, so lenders will demand higher returns to compensate for this. Therefore, if inflation is expected to be higher, bond yields will go up.

Up next, we have the expected path of future short-term interest rates, also known as the “risk-neutral yield.” This is simply an estimate of what government bond yields would be if investors were indifferent to risk. For example, if investors expect short-term rates to move as anticipated with zero uncertainty, they could buy a government bond that matures in ten years, or they could buy a new 1-year bond every year for ten years, it wouldn’t matter.

But, of course, there are risks involved in holding a longer-term bond versus shorter-term ones. And because of these risks, investors will demand a term premium in compensation. In essence, the term premium is the compensation investors require to bear the risk that short-term rates don’t evolve as expected.

According to former Federal Reserve Chairman Ben Bernanke, unexpected inflation has historically been the most important risk for long-term bondholders and is thus the biggest driver of the term premium.

This might explain what we see currently in the bond market. In March of last year, the term premium was actually negative and at its lowest point ever. Fast forward to today, however, and the term premium is a positive 0.6%—its highest level in more than four years. For various reasons, investors are less sure about the prospects of future inflation, so they are demanding higher long-term rates to compensate for this risk.

The bottom line is that even though short-term rates are expected to be held down by the Fed in the foreseeable future, as demonstrated by the low risk-neutral yield, rising uncertainty (particularly around future inflation) is leading investors to require higher long-term rates to offset the risk of uncertainty.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.